COVID-19 & Stock Market Volatility in Nigeria: Would Equity Derivatives Have Made Any Difference?

Across the world, the coronavirus pandemic has continued to wreak havoc not only on lives but also on livelihoods.

Stock markets, useful barometer for economic health, have been roiled not least because of the uncertainty associated with COVID-19.

As of May 22, 2020 (the day of penning this article), major stock markets were already gasping for breath. Market-Watch reports that apart from the tech-heavy NASDAQ composite index which was up 3.92%, Year-To-Date, for understandable reasons (the crisis is setting new normal that tends to benefit the technology sector), other global stock market performance indicators were in the negative territory.

These include the Dow Jones Industrial Average, an index of 30 blue-chip United States stocks, which was down by -13.88% and the S&P 500 index that has plummeted by -8.52% since the beginning of 2020.

In Europe, according to Trading Economics, the UK FTSE 100 index, which tracks the performance of one hundred most capitalized companies traded on the London Stock Exchange, is down -20.65; Germany DAX 30 stock market index has tanked by -7.35, while France CAC 40 stock market Index is -15.84% in the red.

In Asia, Japan Nikkei 225 index has plunged by -13.82% while China Shanghai composite market index has lost -7.75% of its value since January this year according to Bloomberg.

In response, many stock exchanges are altering trading rules to deal with intense volatility occasioned by uncertainties associated with COVID-19.

For instance, short-selling was suspended by market regulators for a period of time in Greece, Italy, Spain, France, Turkey, India and South Korea, while Thailand, South Africa and Indonesia witnessed the activation of circuit-breaker rules.

Indeed, COVID-19 is having an unprecedented adverse impact on global stock markets and Nigeria is no exception. As of May 22, the YTD of the Nigerian Stock Exchange All Share Index was -6.10% down from 7.46% on 31 Jan 2020.

What is more worrisome is the attendant volatility due to growing uncertainty regarding the duration of the pandemic and the scale of its devastation on the economy.

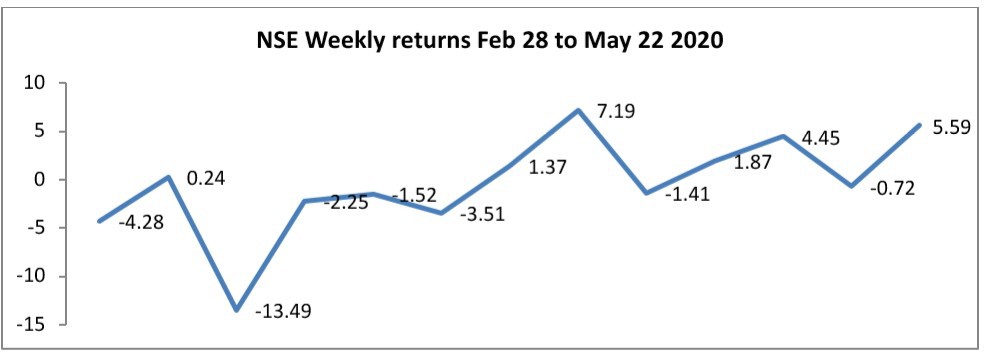

The intensity of the volatility can be seen from the V-shaped nature of the Nigerian Stock Exchange weekly stock market returns between the 27th February when the index case was announced in Nigeria and 22nd May 2020.

While the second week of March which ended on the 13th witnessed the deepest plunge of -13.49%, the second week of April that closed on the 17th recorded the highest weekly returns of 7.19%.

Source: NSE weekly stock market reports

As always, the elevated volatility in the Nigerian stock market is a major disincentive for institutional investors, such as pension funds and mutual funds that are relatively less active in the equities market with asset allocation concentrated in government bonds and Treasury bills generally considered less volatile.

Empirical studies confirm that equity derivative is crucial in tackling market volatility and deepening the stock market. As a matter of fact, while COVID-19 is taking a toll on developed and emerging markets, its impact on countries like South Korea and China is limited by the presence of robust equity derivative markets that are helping investors mitigate losses.

In Nigeria, trading in equity derivatives is still on the drawing Board. Would it have made any difference in the stock market performance if it were in place?

To be sure, a derivative is a contract that derives its value from the performance of an underlying asset, such as equities, bonds, currency and commodities.

Exchange-traded derivatives are derivatives with standardised contracts such as futures and options, while OTC derivatives are products other than exchange-traded ones, such as forwards and swaps.

Indeed, like other family of derivatives, equity derivatives can offer certain important benefits including risk reduction, liquidity enhancement of the underlying asset, aiding price discovery and facilitating portfolio management as a cocktail of products fosters investment diversification.

According to The Futures Industry Association (FIA), since the beginning of this year, ‘global derivatives markets have absorbed increasingly large waves of trading volume and volatility.

Panic about the economic impact of the coronavirus outbreak and a huge drop in oil prices have sparked extreme market volatility, encouraging investors to find ways of hedging risk with products such as stock index futures and equity options’.

In China for example, the importance of equity derivatives as a hedging tool has been growing in the wake of COVID-19. In recognition of the vital role of equity derivatives in mitigating investors’ losses, the China Securities Regulatory Commission broadened the derivatives market by approving the launch of five commodities options and three financial options in a bid to attract more global investors to China with an eye on Hedge funds. And the move is paying off.

According to Reuters, ‘’Trading in China’s equity derivatives has hit a five-year high with some products seeing record volume in a sudden comeback for a market considered essential in other major economies.

Trading in stock index futures has hit its highest since the end of 2015 with nearly $70 billion worth of contracts changing hands each day while stock option trading has set records with the number of open contracts exceeding 5 million on the Shanghai Stock Exchange’’.

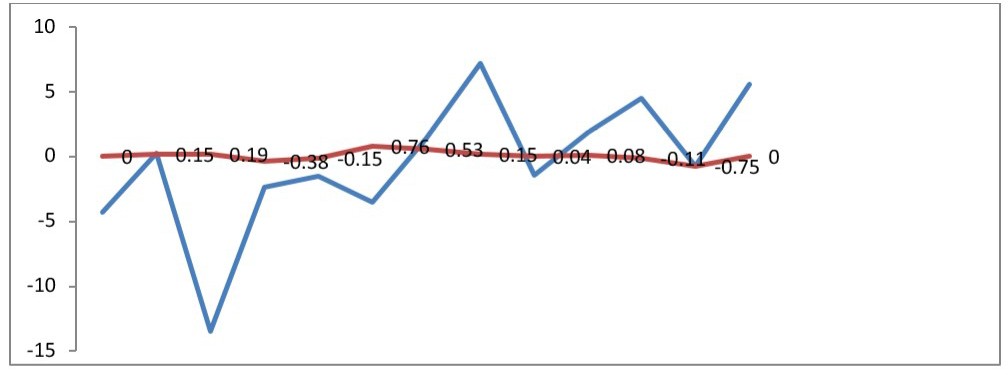

So, it goes without saying that in China, equity derivatives has helped to mitigate stock market volatility in a country that first came under the attack of the dreaded SARS-COV2.

This is evident in the relatively flat shape of the Shanghai composite weekly returns when compared to the V-shaped weekly returns on the Nigerian Stock Exchange between February 28 and May 22 2020.

Source: Trading Economics and NSE weekly stock market reports

By the same token, the use of equity derivatives in South Korea has assisted firms and financial institutions to hedge the risk of losses from volatility of stock prices due to COVID-19.

Statista reports that as of May 22, 2020, South Korea had confirmed 11,142 cases of infection including 264 deaths after the first case of coronavirus in the country on January 20, 2020.

According to the Futures Industry Association, listed futures and options contracts tied to the KRX KOSPI 200, which is the South Korea Exchange’s main benchmark stock index, have remained the world’s most-traded derivatives contracts.

Several positive factors are contributing to the growth of the derivatives market in Korea according to the country’s Financial Supervisory Service. These include information sharing between the spot and derivatives market and the ability of regulators to take swift and reliable emergency measures to cope with sudden market fluctuations employing market stabilisation schemes, such as circuit breakers, trading halts and daily price fluctuation limits.

For instance, On March 12, 2020, The Korea Exchange activated a “sidecar trading curb,” temporarily halting the trading of shares, for five minutes, after KOSPI 200 index futures fluctuated 5% from the previous close.

This is in addition to strong governing laws and regulations in respect of market price manipulation which cover entry regulations, prudential regulations, investor protection and market surveillance.

On investor protection for instance, there is a regulation that provides that ordinary/retail investors, in addition to minimum margin requirements, are also required to comply with education and mock trading requirements.

All said, while the full impact of COVID-19 on stock markets may not be known, what seems not in doubt is that equity derivatives have been useful as hedging tools in mitigating investors’ losses from market volatility.

It is against this backdrop that the progress made by the Securities and Exchange Commission and the Nigerian Stock Exchange in the area of increasing the menu of available asset classes for investors in the Nigerian capital market via equity derivatives deserves commendation.

It bears repeating that the expansion of offerings in the Nigerian stock market will improve risk management tools and enhance the allure of the market for meeting hedging needs especially to global investors who, not a few believe, are still underweighted on Nigerian stocks.

Without a doubt, in an era of volatile stock markets occasioned by COVID-19 pandemic, options and futures can provide investors more strategies. Hence, equity derivatives would surely have made a positive difference in the Nigerian Stock market.

Uwaleke is a Professor of Capital Market at the Nasarawa State University Keffi